Production gets completed.

Materials are issued.

The order is delivered.

The customer receives the finished product.

At that point, many businesses consider the job complete.

But one important question often remains unanswered:

How much material was actually consumed to produce that order?

The answer matters more than it may initially appear.

Because material consumption influences inventory accuracy, product costing, purchasing decisions, and ultimately profitability.

Without visibility into actual consumption, businesses can continue producing and delivering successfully while slowly losing control over costs.

Material Variance Explained in Simple Terms

Material variance is the difference between what was expected to be consumed and what was actually consumed during production.

Consider a simple example.

A production process estimates that 100 grams of material are required to produce a unit.

Once production is completed, the actual consumption is found to be 115 grams.

The variance is 15 grams.

The additional consumption may not appear significant for a single unit.

However, when production volumes increase, even small variances can have a measurable impact on inventory levels and production costs.

The variance itself is not necessarily a problem.

The challenge begins when nobody knows why it happened.

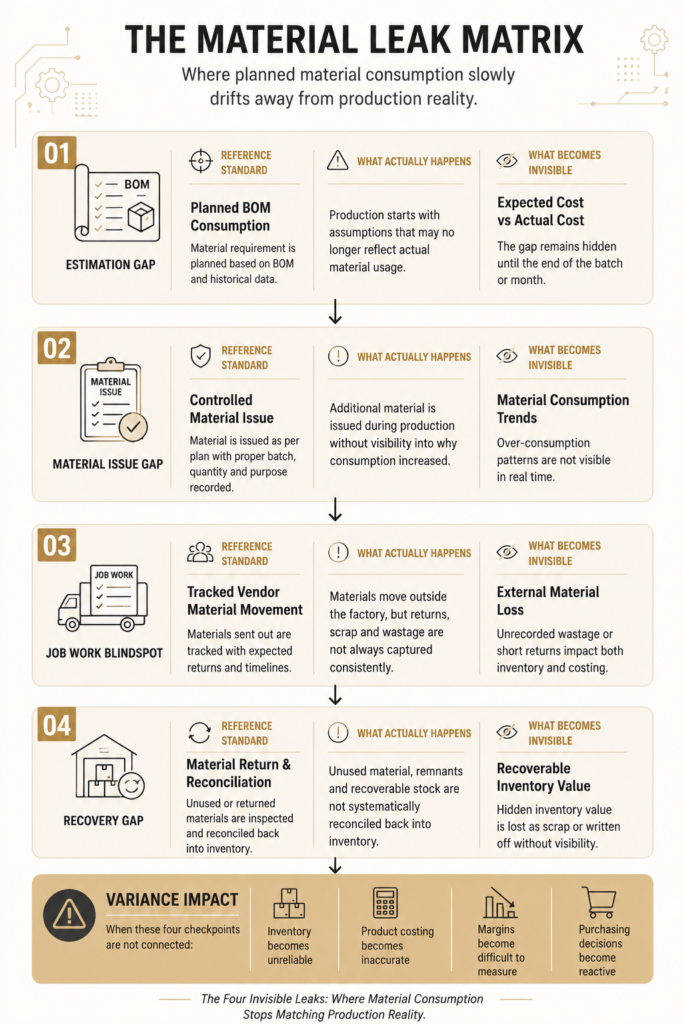

Where Material Variance Usually Starts

Material variance often originates much earlier than people expect.

It can begin during:

- Material planning

- BOM preparation

- Material issue to production

- Job work allocation

- Production execution

- Material returns

In many manufacturing environments, materials are issued to a production team, operator, or external vendor.

At completion, some materials may be consumed, some may be returned, and some may become wastage.

If these movements are not tracked properly, visibility starts to fade.

Eventually, stock records, production records, and actual material consumption begin telling different stories.

A Practical Example from Textile Manufacturing

Consider a weaving operation where silk thread and zari materials are issued to produce a saree.

The issued quantity is known.

The finished product is delivered.

Unused thread is expected to be returned.

From a business perspective, the important questions are:

- How much material was originally issued?

- How much was actually consumed?

- How much was returned?

- How much became wastage?

- What was the actual material cost of producing the saree?

Without clear answers, product costing becomes an estimate rather than a reliable number.

As production volume increases, these small gaps become increasingly difficult to track manually.

Why This Matters Beyond Inventory

Material variance is often viewed as an inventory issue.

In reality, it affects several parts of the business.

Product Costing

If actual consumption consistently exceeds planned consumption, product costs rise.

Without visibility into this trend, pricing decisions may continue to rely on outdated assumptions.

Inventory Accuracy

When consumption and returns are not tracked accurately, stock records gradually drift away from reality.

Teams begin relying on physical verification rather than system information.

Purchasing Decisions

Procurement planning becomes difficult when actual consumption patterns are unclear.

Materials may be ordered too early, too late, or in incorrect quantities.

Margin Visibility

A product that appears profitable on paper may deliver a much lower margin once actual material usage is considered.

Without tracking variance, these issues often remain hidden.

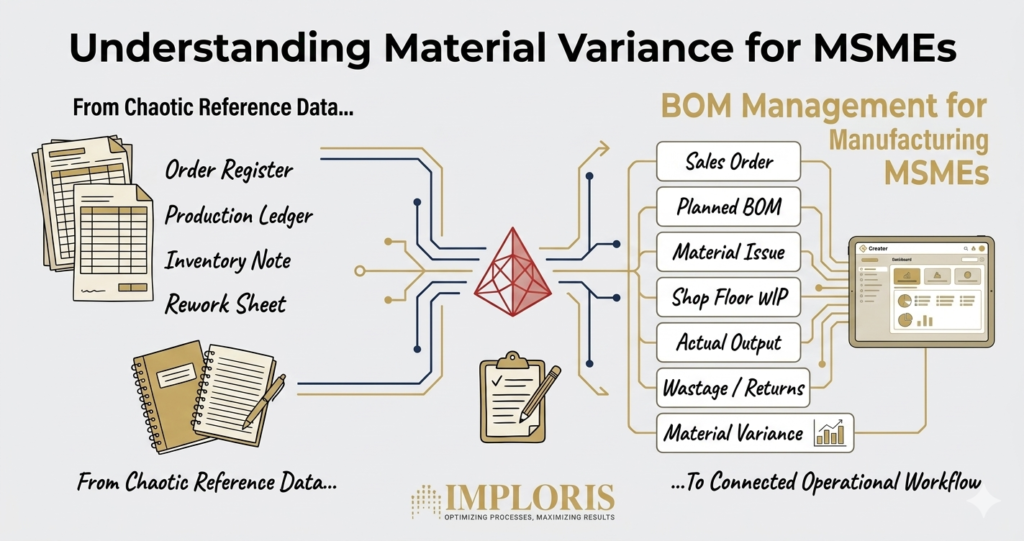

The Visibility Problem

The challenge is rarely the absence of data.

The challenge is that information exists in multiple places.

Material issue registers.

Excel sheets.

Production slips.

Ledger books.

WhatsApp messages.

Individual follow-ups.

Each record may contain part of the story.

What is often missing is a single view that connects them together.

This makes it difficult to answer simple operational questions:

- What was issued?

- What was consumed?

- What was returned?

- What was wasted?

- What was the final material cost?

By the time answers are gathered, the next production cycle has already started.

Material Variance Is Often a Process Signal

An increase in material consumption does not automatically indicate a problem.

Sometimes it reveals useful information.

For example:

- A BOM may no longer reflect actual production requirements.

- A process may require refinement.

- Material quality may have changed.

- A supplier may be delivering inconsistent inputs.

- Additional wastage may be occurring at a particular stage.

Variance provides a signal.

Understanding that signal allows businesses to improve processes, planning, and forecasting.

Ignoring it simply allows the same issue to repeat.

Connecting Material Tracking to Production Visibility

Material variance becomes easier to manage when material movement is connected to the broader production workflow.

This includes visibility into:

- BOM requirements

- Material issues

- Production execution

- Job work activities

- Work-in-progress tracking

- Material returns

- Finished goods output

When these activities are connected, businesses can move beyond assumptions and work with actual operational data.

The objective is not to create additional administration.

The objective is to create clarity.

How We Approach This at Imploris

We do not begin with software.

We begin by understanding how materials move through the business.

That includes:

- how materials are received

- how they are issued

- how production is tracked

- how returns are recorded

- how wastage is identified

- where visibility is currently being lost

From there, we design workflows around the process and implement the required structure using Zoho Creator and supporting Zoho applications where appropriate.

The goal is not simply to record transactions.

The goal is to create operational visibility that supports better decisions.

Closing Thoughts

Material variance is not just a production metric.

It is a visibility metric.

When businesses understand the relationship between planned consumption and actual consumption, they gain a clearer picture of inventory, costing, purchasing, and profitability.

The conversation is no longer about whether material was consumed.

The conversation becomes understanding where it went, why it was consumed, and what can be improved going forward.

If material consumption, stock levels, and production costs do not always align, it may be worth reviewing how materials are currently being tracked across the production cycle.

A focused discussion is often enough to identify where visibility is breaking and what a more structured approach could look like.